-

Table of Contents

Understanding $80,000 After Tax in the U.S.: A Comprehensive Guide

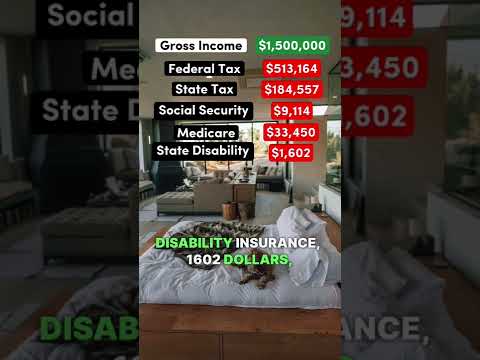

In today’s economy, understanding your take-home pay is crucial for effective financial planning. For many, an annual salary of $80,000 is a significant milestone. However, the amount you actually take home after taxes can vary widely based on several factors, including your state of residence, filing status, and deductions. This article will explore what $80,000 translates to after tax in the U.S., providing insights into tax brackets, deductions, and practical financial implications.

Breaking Down the Tax Brackets

The U.S. federal income tax system is progressive, meaning that as your income increases, so does the rate at which you are taxed.

. For the tax year 2023, the federal tax brackets are as follows:

- 10% on income up to $11,000

- 12% on income over $11,000 to $44,725

- 22% on income over $44,725 to $95,375

- 24% on income over $95,375 to $182,100

For an individual earning $80,000, the federal tax calculation would look something like this:

- 10% on the first $11,000 = $1,100

- 12% on the next $33,725 (from $11,000 to $44,725) = $4,047

- 22% on the next $35,275 (from $44,725 to $80,000) = $7,760.50

Adding these amounts together gives a total federal tax liability of approximately $12,907.50. This means that your take-home pay before any state taxes or deductions would be around $67,092.50.

State Taxes: A Variable Component

In addition to federal taxes, state taxes can significantly impact your take-home pay. Each state has its own tax rates and brackets. For example:

- California: Progressive rates ranging from 1% to 13.3%

- Texas: No state income tax

- New York: Progressive rates ranging from 4% to 10.9%

For someone earning $80,000 in California, the state tax liability could be around $3,000, while in Texas, it would be $0. This difference can lead to a substantial variation in take-home pay.

Deductions and Credits: Maximizing Your Take-Home Pay

Tax deductions and credits can further influence your final tax bill. Common deductions include:

- Standard deduction (for 2023, $13,850 for single filers)

- Itemized deductions (mortgage interest, medical expenses, etc.)

- Retirement contributions (401(k), IRA)

For instance, if you take the standard deduction of $13,850, your taxable income would drop to $66,150. This would reduce your federal tax liability and increase your take-home pay. Additionally, contributing to a retirement account can lower your taxable income further.

Real-Life Example: Case Study of Two Individuals

To illustrate the impact of state taxes and deductions, consider two individuals:

- John: Lives in Texas, takes the standard deduction.

- Jane: Lives in California, takes the standard deduction.

For John:

- Federal tax: $12,907.50

- State tax: $0

- Take-home pay: $67,092.50

For Jane:

- Federal tax: $12,907.50

- State tax: $3,000

- Take-home pay: $62,092.50

This example highlights how location and tax strategies can significantly affect your financial situation.

Conclusion: Key Takeaways

Understanding your take-home pay after taxes is essential for effective financial planning. With an annual salary of $80,000, various factors such as federal and state tax rates, deductions, and credits can influence your final amount. Here are the key takeaways:

- Federal tax brackets are progressive, meaning higher income is taxed at higher rates.

- State taxes can vary significantly; some states have no income tax at all.

- Deductions and credits can help lower your taxable income and increase your take-home pay.

By being informed about these factors, you can make better financial decisions and maximize your earnings. For more detailed information on tax brackets and deductions, you can visit the IRS website.